By: Mary C. Lacity and Leslie P. Willcocks

For the past three years, we have surveyed clients about their service automation journeys during the client-only networking session at the Outsourcing World Summit (OWS). In 2016[i] and 2017[ii], we concluded that Robotic Process Automation (RPA) was happening “now,” Cognitive Automation (CA) was happening “soon,” and Blockchains (BC) were happening “later” for most organizations. This year’s survey of 68 clients attending the networking session at OWS18 in Orlando Florida replicated these timelines, but with signs that RPA was scaling fast and that CA was making steady progress. Although blockchains generated the most interest among client firms, the technology is still immature, with live deployments coming later. We also found that most organizations most frequently use service automation tools to free up human capacity for more interesting work.

About the Authors

Mary C. Lacity is leading a research project to answer the question: How are enterprises preparing for blockchains? She has held visiting positions at the London School of Economics, Washington University, and Oxford University. She is a Certified Outsourcing Professional ®, Industry Advisor for Symphony Ventures, and Co-editor of the Palgrave Series: Work, Technology, and Globalization. She was inducted into IAOP’s Outsourcing Hall of Fame in 2014, one of only three academics to ever be inducted. She has published 27 books, most recently Robotic Process and Cognitive Automation (2018), which will debut at OWS18, as well as Robotic Process Automation and Risk Mitigation: The Definitive Guide (2017) and Service Automation: Robots and the Future of Work (2016) (SB Publishing, UK, co-author Leslie Willcocks).

Leslie P. Willcocks is Professor in Technology Work and Globalization at the Department of Management at London School of Economics and Political Science. Leslie has a global reputation for his work in robotic process automation, AI, cognitive automation and the future of work, outsourcing, global strategy, organizational change, and managing digital business.

Service Automation Adoption

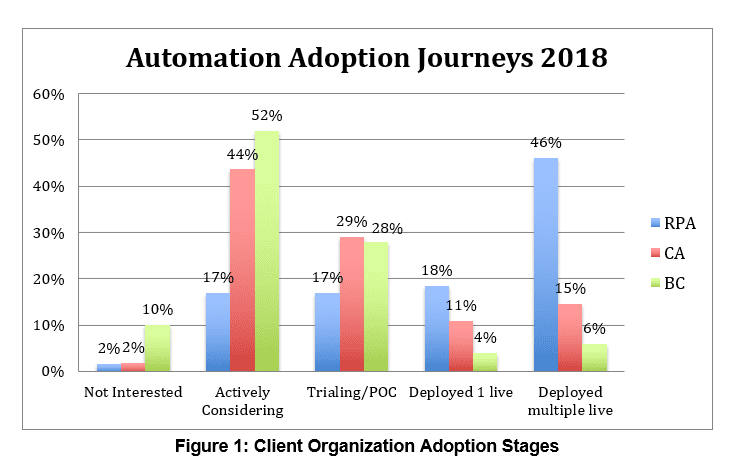

We asked clients to indicate the adoption stages for RPA, cognitive automation and blockchains in their organizations. Among the clients who responded to the question, 64 percent indicated that their organizations had already deployed RPA compared to 37 percent in 2017 (see Figure 1). Furthermore, we have seen a scaling of RPA over the last year, with 46 percent of organizations reporting multiple live RPA deployments. This finding resonates with our extensive case study-based research documented in our recent book.[i] Organizations that thought strategically about RPA and started small to learn quickly scaled quite rapidly in our study. By February 2018 we were seeing a number of case studies where hundreds of software robots were running in production.

46% of Organizations Report Multiple Live RPA Deployments

In contrast to RPA, 26 percent of client organizations had already deployed one or more CA applications, which was up from the 15 percent reported last year. Thus CA adoptions are happening, but at a slower pace than RPA adoptions. Why? Our case study research finds that CA adoptions are more challenging than RPA in several ways. First, there’s the data challenge; whereas RPA dealt with tidy structured data in our case studies, cognitive automation tools were often deployed on unstructured data like text, audio, and images. In order to get the CA tool to properly process unstructured data, thousands of labeled examples were needed to train the CA tool. Second, there’s the price. In general, RPA tools are less expensive than CA tools, so it’s easier to justify the business case for RPA than CA. RPA’s price advantage might diminish as more open source CA tools mature. Third, there’s the unpredictability of outcomes. While all the logic paths of an RPA application can be tested in advance, no organization can predict with certainty how users will interact with a CA tool. For example, at Deakin University, the administrators and staff built a virtual cognitive agent to answer student queries. The university anticipated that students would most frequently ask questions about educational processes, such as how to enroll in classes. In reality, students most frequently asked for information about finding dates, finding food, and the location of course materials — in that order.

Finally, only 10 percent of respondents indicated that their organizations had already deployed one or more blockchain technologies. Even this percentage seems high, as our research at MIT found very few live blockchain deployments.[i] Unlike RPA and CA tools that can be deployed within a firm’s boundaries, the real value of blockchains comes from shared applications among many trading partners. The power of blockchain applications will be unleashed “later,” when industry partners agree on standards for inter-organizational transactions. What is most noteworthy is that over half of the clients in the IAOP survey reported that their organizations were actively considering blockchain technologies.

Business Value Delivered

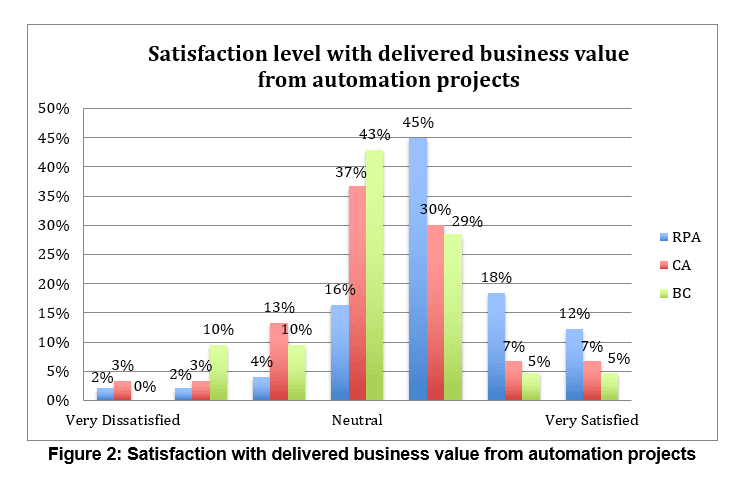

Are service automation deployments generating business value? We asked clients to indicate their level of satisfaction with the business value delivered by their RPA, CA, and BC deployments. We used a seven-point Likert Scale with “1” indicating “very dissatisfied” and a “7” indicating “very satisfied” with the business value delivered. Of those organizations that had deployed, the mean ratings were 5.04 for RPA (somewhat satisfied) and 4.33 and 4.24 (neutral) for CA and blockchain, respectively. However, there is considerable variance (see Figure 2), which resonates with our case study research. We identified over 41 risks that can derail service automation projects. The difference between delivering and failing to deliver value depended more on the management practices applied than on the tools themselves. That said, RPA capabilities vary across tools and platforms; their distinctive attributes shape what can and cannot be done, and the amount of management and technical effort needed to scale.

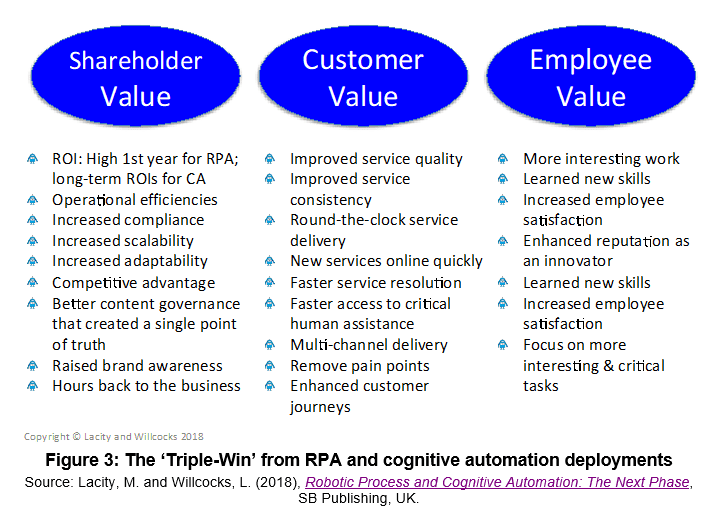

In our case study research, successful automation projects delivered a triple-win of value for shareholders, customers, and employees (see Figure 3). They did so by applying sound action principles to strategy formulation, sourcing selection, tool selection, project selection, stakeholder buy-in, change management and built a resilient, secure operating environment to run and scale automations.

Sourcing for Service Automation

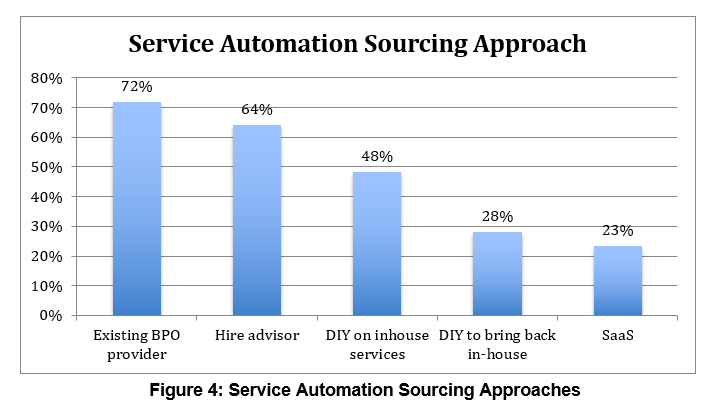

We next asked clients which sourcing approach they typically used for service automation programs. Clients most commonly reported that they relied on their current service providers to automate services for them (see Figure 4). This is good news for business and IT service providers that have developed significant automation capabilities. For clients, the benefits of engaging a traditional provider include a full suite of integrated services that combine labor arbitrage, process excellence, change management maturity and technology expertise. The downside is provider-lock in. If a client wants to switch providers, it may find it needs to recreate the automations with the new provider.

Advisors will also be pleased to learn that 64 percent of clients said they hire advisors to help with service automation. In the past few years, we have seen advisors quickly building service automation practices in response to increased client demand. Advisory firms track the service automation landscape and help clients with their service automation journeys. Credible advisors need to master a variety of tools to be “tool agnostic,” and they must understand which tools are best suited to meet a client’s needs. Advisors are building capabilities by a variety of means. These include: adopting tools to automate their own internal services, hiring pioneers from early enterprise adopters, and sending analysts through the software provider’s training certification programs.

Nearly half of clients also manage some automation programs themselves, without outside help from providers or advisors. With insourcing, client organizations bear all the risks of service automation themselves but earn all the benefits — if managed well. For this “do-it-yourself” (DIY) model to pay off, clients need to invest significant resources in building internal service automation skills.

A smaller percentage of client organizations use service automation to bring services back in-house (28 percent) or are beginning to buy automations as a service (SaaS) (23 percent). Both of these percentages are double last year’s figures. Ian Barkin, Chief Strategy Officer for Symphony Ventures, sees these trends as related, saying:

“Technology has evolved quickly, but organizational change and contract timelines prevent similar paces in operations. However, several years into RPA, we’re seeing interesting behaviors surfacing. First, free agent status is spreading as five and seven-year BPO contracts are coming due. Firms are liberated to consider their options – and they have so many new and interesting options! Second, firms are repatriating because ‘cheap’ was compelling, but they now know there’s more to value than just lower cost – they are looking to bring work back, closer to the core, and automation makes that possible. Third, comfort with the cloud is bedding in.”

The SaaS model is a particularly interesting trend to watch, as increasingly clients are interested in hiring providers to “manage robots,” typically with three-year SaaS contracts. Clients like the “pay-as-you-use” model of a virtual workforce. Barkin continued, “SaaS is not just for Customer Relationship Management (CRM) anymore. Increasingly, firms are looking to migrate to a ‘Digital Operation’ that is integrated, orchestrated, and innovated on their behalf. This perfect storm of free agency, value realignment and comfort with SaaS models promises to have truly profound effects on how work is done.”

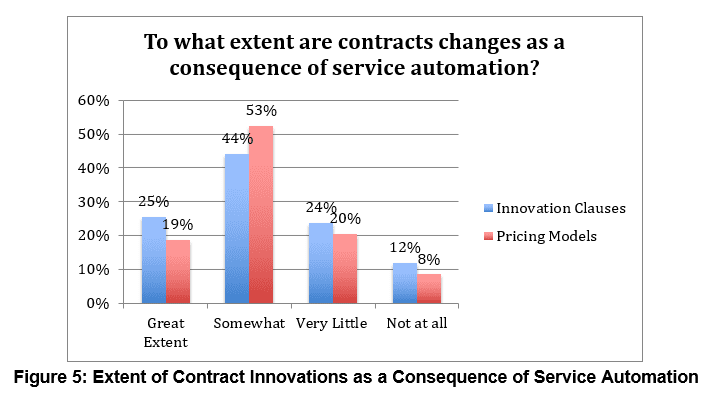

Automation Innovations Outpace Contract Innovations

This year we asked clients the extent to which their contracts were changing to keep pace with advances in automation. Specifically, we asked whether innovation clauses or pricing models were different as a direct consequence of service automation. Overall, the majority of clients reported that contracts were being changed only “somewhat” (see Figure 5).

Only a quarter of the clients reported that they were substantially revising their innovation clauses because of service automation. Only 19 percent reported changing their pricing models to a great extent. No matter how much clients, providers, and advisors agree that FTE rate cards are a poor pricing model, their stickiness pervades. FTE rate cards are indeed the simplest way to size a service, but as an input metric, it does little to capture the real value delivered by services. As a community, we have long debated the need for new pricing models, and it’s time for a more serious study of what actually works.

Automation and Excess Labor Capacity

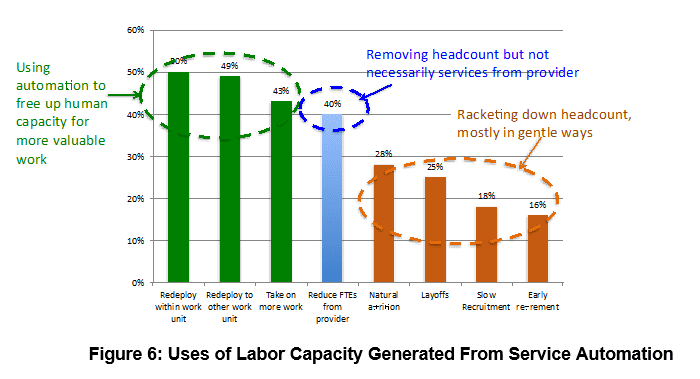

Amidst the fears that automation could lead to a “jobless future,” we have always answered the question, “Does service automation lead to massive layoffs?” with empirical data. On the OWS18 survey, we asked respondents, “What does your organization do with the FTE savings generated from automation?” For the 68 clients who responded to this question (see Figure 6), the most common responses were redeploying employees within the unit (50 percent), redeploying employees to other work units within the company (49 percent), and taking on more work without adding more people (43 percent). These three common uses indicate that service automation is being used to create excess human capacity to focus on more value-added work. Leslie Willcocks has called the phenomenon, “using service automation to take the ‘robot’ out of the human.” Across multiple case studies, we found organizations automating the dreary and repetitive tasks so that employees can focus on what they were better hired to do, like solve problems, think creatively, and build relationships.

Forty percent of clients also use service automation to reduce the number of provider FTEs servicing their accounts. As we saw in the previous section, many clients rely on their service providers to improve services using automation technologies, so the reduction in provider FTE headcount does not indicate a decline of outsourcing for most client organizations. Instead, it means that service providers have made significant investments in automations that allow them to provide services to clients with fewer people.

Finally, as organizations start scaling their automations, they may need fewer people. However, the preferred methods gently racket down headcounts through natural attrition, by slowing recruiting, or by offering early retirements. Only 22 percent of client firms reported layoffs as a consequence of service automation.

Conclusion

By 2018 RPA, cognitive automation and blockchains had reached interesting stages. The RPA market is likely to expand by at least 38 percent compound annual growth over the next five years. Cognitive automation deployments are still immature and much fewer in number but are forecasted to start taking off at the back end of 2018. Whereas RPA and CA tools can be deployed within enterprises to produce the triple-win of value, blockchains are tools designed for inter-organizational transactions and will, therefore, require significantly more effort to define standards, build shared governance models, and gain a critical mass of adopters. In our new books, we document the emerging challenges of RPA, cognitive automation and blockchain deployments. It is clear that many companies find scaling a problem across all three technologies.

In Robotic Process and Cognitive Automation: The Next Phase, we found that many firms did not put in place the necessary governance, and often did not use tools that contain built-in technical controls. An RPA and CA skills shortage is already upon us, affecting all players, not just clients’ internal capabilities. RPA was often under-funded, and senior management was guilty too often of not taking a strategic approach. Stakeholder buy-in and change management were not really getting the attention they deserved. None of this is helped by over-claims of what some RPA tools can do, as opposed to their real “out-of-box” functionality. As we document in our book, there are many over-claims on the ability to provide comprehensive cognitive automation, as opposed to discrete tools that can fit with some RPA deployments. Meanwhile, though high in the headlines, practical examples of so-called “Artificial Intelligence” — “getting computers to do what minds can do” — are notably absent from the vast majority of our workplaces, globally.

In A Manager’s Guide to Blockchains for Business: From Knowing What to Knowing How, we found a tremendous amount of experimentation with thousands of proofs-of-concepts across industries and geographies, but with very few live blockchain deployments because of technical and non-technical challenges. Executives interviewed for this research were confident the cadre of bright people in working groups and startups would successfully address the technical challenges. They were more concerned with the required mind-shifts, new shared governance models, standards, and regulatory challenges that need to be addressed before more blockchain applications can be widely deployed and scaled.

All this is likely to change over the next two years, and we look forward to finding with IAOP members, new case studies of success, and identifying perennial and fresh action principles for managing these emerging automation technologies.

Mary Lacity and Leslie Willcocks’ books are available from www.sbpublishing.org.

[i] Lacity, M. and Willcocks, L. (2016), “Speed of Automation Adoption Faster for Providers than Customers,” Pulse Magazine, May/June, pp. 10-17.

[ii] Lacity, M., Babin, R., and Willcocks, L. (2017), “Research Center: Service Automation Trends Survey,” Pulse Magazine, Issue 28, pp. 40-44.

[i] Lacity, M. and Willcocks, L. (2018), Robotic Process and Cognitive Automation: The Next Phase, SB Publishing, UK.

[i] Lacity, Mary, Moloney, K., and Ross, J. (2018), “Blockchains: How to position your company for the inevitable,” MIT CISR Research Briefing.

Lacity, M. (2018), A Manager’s Guide to Blockchains for Business: From knowing what to knowing how, SB Publishing, forthcoming